Employee Provident Fund: Structure and Rates

PF Contribution – Calculation Overview

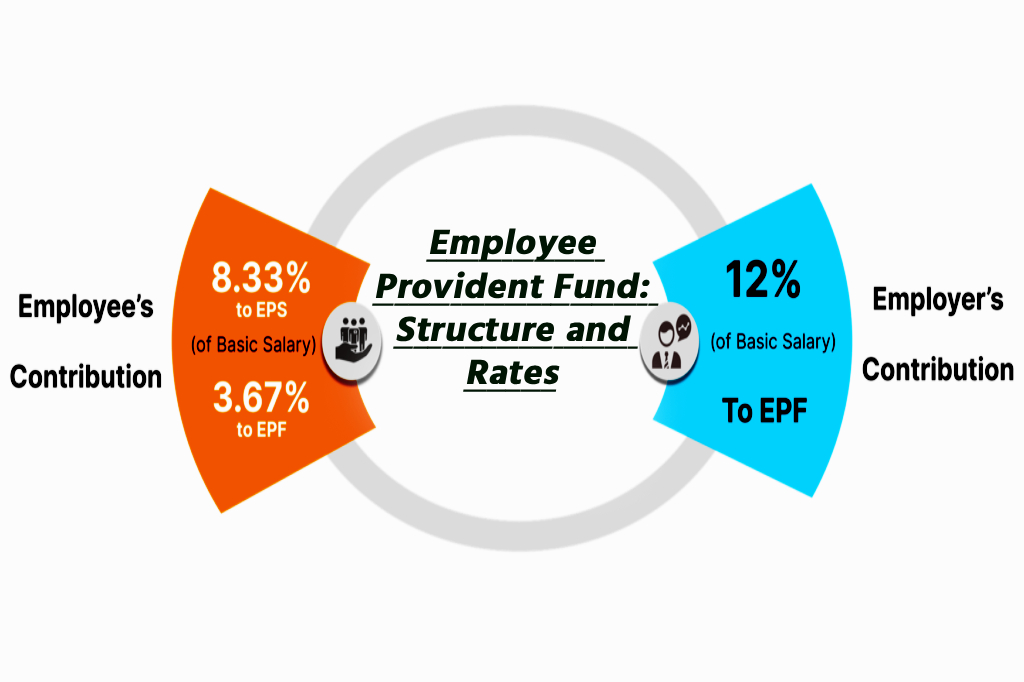

The Employee Provident Fund (EPF) is a retirement savings scheme mandated by the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952. Both employers and employees contribute towards this fund as follows:

- Employee Contribution: Usually 12% of basic salary plus dearness allowance (DA). In establishments with fewer than 20 employees or in specified sectors like Jute, Beedi, etc., the contribution rate is 10%.

- Employer Contribution Breakdown:

- 8.33% directed towards the Employees’ Pension Scheme (EPS).

- 3.67% credited to the Employee Provident Fund (EPF).

- 0.50% towards Employees’ Deposit Linked Insurance (EDLI).

- 0.50% administrative charges (effective since July 2018).

Interest Rate

- The EPFO sets the interest rate annually, subject to approval by the Ministry of Finance.

- Recent rates:

- 2018–19: 8.65%

- 2017–18: 8.55%

- Interest is calculated monthly on the account’s running balance and credited annually.

Salary Limit and Eligibility

- EPF contributions are generally calculated on salaries up to ₹15,000 per month.

- Employees earning above this threshold can choose to opt out of EPF contributions upon joining, subject to mutual consent.

Universal Account Number (UAN)

- A unique identifier assigned to each employee by the EPFO.

- The UAN links multiple PF accounts held by the employee across different employments.

- Upon job changes, employees must provide their UAN to the new employer using Form F-11 for seamless transfer of accounts.

Withdrawal Provisions

- Full EPF withdrawal is permitted upon reaching 58 years of age.

- Partial withdrawals or reduced pension benefits can be claimed between 50 and 58 years via Form 10D.

- Employees with less than 10 years of service can withdraw both EPF and EPS balances.

- Withdrawals are processed through the Composite Claim Form.

Taxation of EPF

- Contributions: Employee contributions are tax-exempt up to ₹1.5 lakh under Section 80C. Employer contributions are exempt up to 12%.

- Interest: Taxable if the interest rate exceeds 9.5%.

- Withdrawal: Tax-free if continuous service exceeds 5 years; otherwise, taxable under certain conditions.